Markets, Oil, and the Opportunities Hidden in the Chaos

by Zachary Mineur, CFA, CFP®, Chief Investment Officer at Independence Square Advisors

Buttercup: [worried] “We’ll never survive!”

Westley: [confident] Nonsense! You’re only saying that because no one ever has.

Into the Fire Swamp we go. Or maybe we’ve been here all along. Hard to tell these days. After several revisions to this letter as circumstances swung wildly from one end of the pendulum to the other, it appears that a temporary ceasefire in the Iran war has been agreed to. Something tells me this isn’t the last twist in this tale.

The Iran Conflict: A Gambit with Higher Stakes Than Anyone Planned For

The specter of a potential all-out conflict with Iran has been lurking in the background of American politics for decades. Multiple successive administrations have issued threats, placed sanctions, and engaged in proxy wars against the Islamic Republic. The regime has brutalized its own citizens, funded terrorism abroad, and continued to work towards obtaining a nuclear deterrent. With that backdrop, the current moment feels inevitable in hindsight, though it induces no less anxiety. Perhaps precisely because this conflict hasn’t been ‘solved’ by previous presidents, the current administration has decided to play with the cards in hand, attempting to significantly reorganize the balance of power in the Middle East at what is proving to be a critical chokepoint for the energy needed to fuel the modern global economy. It is a gambit that was likely encouraged by the success of the single-day semi-regime change operation in Venezuela, that made our military look good and induced the government there to be more amenable to American interests. It is safe to say more than a month into this Iranian ‘expedition’ that the stakes are much higher, and it couldn’t possibly be going to plan.

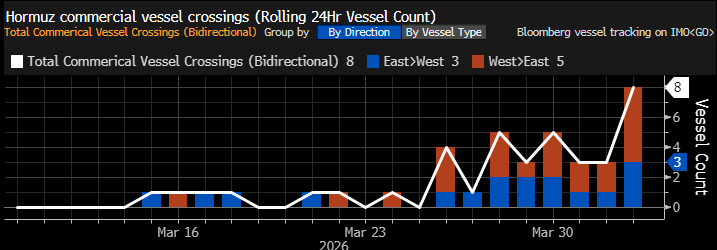

The Strait of Hormuz: More Than Oil Flows Through Here

The world consumes 100 million barrels of oil every single day. 20 million of those barrels flow through the Strait of Hormuz. That flow has essentially been reduced to a trickle.

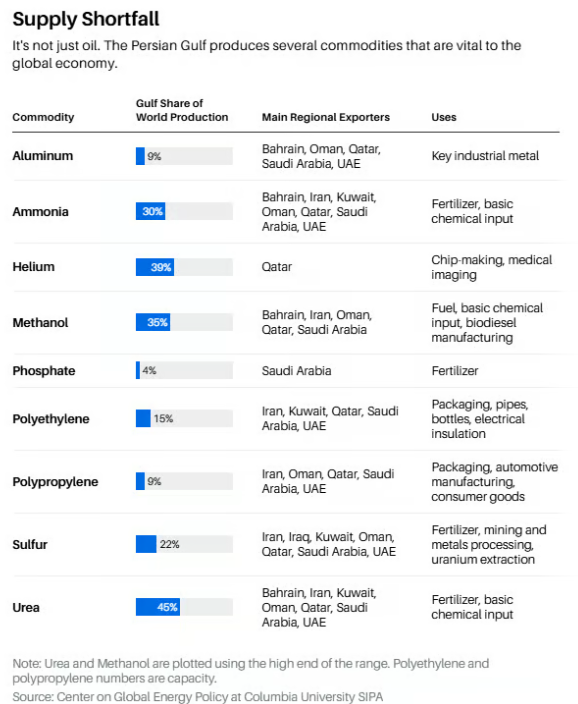

But it isn’t just oil and natural gas that flow through that corridor. Several other commodities that are critical to the global economy have been blocked behind the threat of drones or missiles. Nearly 40% of the globe’s helium passes through the Strait, a required component in the semi-conductor manufacturing that keeps our digital economy plugged in. Up to a third of the world’s supply of Ammonia and Urea pass through the Strait, essential raw materials used in fertilizer needed to grow enough food for 8 billion people.

The attacks by Iran on the industrial facilities in the Gulf threaten long-term supply disruptions to these critical inputs. On top of that, the potential for attacks on the Gulf state’s desalinization facilities represent an existential risk to their countries.

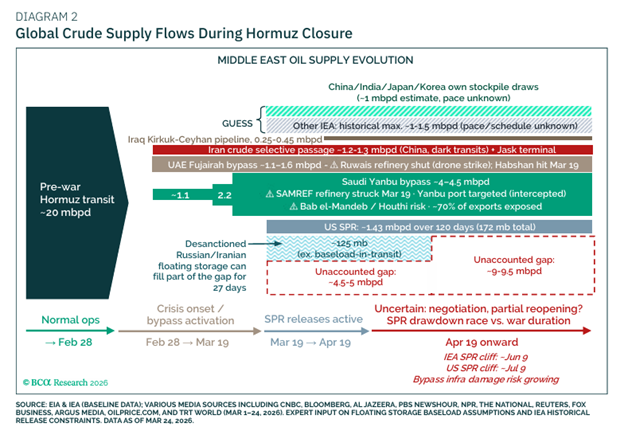

The Supply Gap Is Now Permanent — Until It Isn’t

Oil tankers move at 10-15 knots. For those of you not familiar with maritime terminology, that is about the cruising speed of a bicycle on a Saturday afternoon. Because of this, there was more than a month’s worth of oil already at sea in transit by the time the war commenced and so only now in mid-April are we starting to feel the true effects of a reduction in supply.

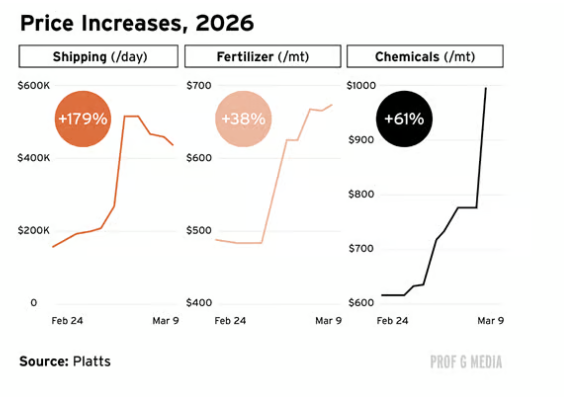

Prices downstream of these raw materials predictably shot up over the past month.

The demand for many of these raw materials, especially oil, is inelastic and not replaceable from other sources. Below we have a chart depicting the various additional production that can be brought online, reserves that can be drawn on, and detours that can be taken to bring additional oil to market. By April 19th, the reserves are drawn down and a permanent gap of 9 – 9.5 million barrels per day persist. There is just nowhere else to turn to replace that production.

What Iran Just Proved to the World

Even if the conflict is resolved before any long-term supply disruptions are realized this conflict has unearthed and proved effective a “known unknown” that has the potential to significantly disrupt the global economy. We have always known implicitly that this was possible. What wasn’t known by anyone, including the Iranians, is whether they could do it sustainably while under the full pressure of the US military from the air and with only a handful of inexpensive drones and relatively inexpensive missiles. They, and the world, now know that they can. Everyone also knows that short of an all-out ground offensive, we can’t really stop it.

The Iranian regime has proven resilient in the face of superior military firepower, multiple assassinations of top leaders, and bubbling domestic resentment, which was brutally put down earlier in the year. Estimates suggest that more than 30,000 civilian protesters were killed before the war began. Despite everything working against them, they have been able to keep the Strait closed under threat of drone and missile attacks and demonstrated they can inflict severe damage on Gulf energy infrastructure.

The administration faced the decision to either escalate further to reopen the Strait by force, of which the options are uncertain and come with significant risk to US personnel, or risk a Strait that will operate under Iranian control, the nature of which will be whatever they decide it is. Will they charge tolls? Only let vessels from certain countries go through? Extract concessions from Gulf states to get their products out to the world? Will there be some grand bargain struck that can pull all parties out of the swamp? At this point, I suppose anything is possible, but the options all look rather unappealing.

The Bear Playbook, the Ceasefire Rally, and What Comes Next

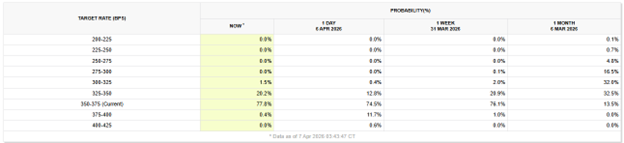

Along with higher commodity prices and the possibility of resurgent inflation, the market’s expectations for Federal Reserve monetary policy has shifted dramatically to a more hawkish position, now pricing in a 73% probability of no rate cuts at all this year. We can see that one month ago (far right-hand column), there was nearly a 90% probability of at least one rate cut.

The playbook for the markets in prior bouts of Trump induced volatility has been to buy the dip. For bears, the scarring of last year’s vicious snap-back rally is fresh on the mind, when on April 9th, the President paused his reciprocal tariff programs and the S&P 500 surged 9.5% in a single day. Not a good day to be out of the market and God forbid, short. With the index down for five of the last six weeks and 10-year Treasury yields ticking back up to nearly 4.4%, if you were looking for a repeat of last year’s episode, the conditions were in place that would make that a distinct possibility. And indeed, after much of this note was written, nearly a year to the day, a two-week ceasefire looks likely to make that rally a reality, at least for now.

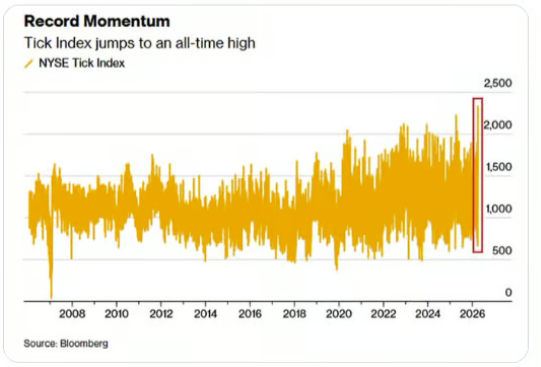

Investors largely followed the playbook. The NYSE showed record momentum on 3/31 with nearly every stock on the exchange up on the day.

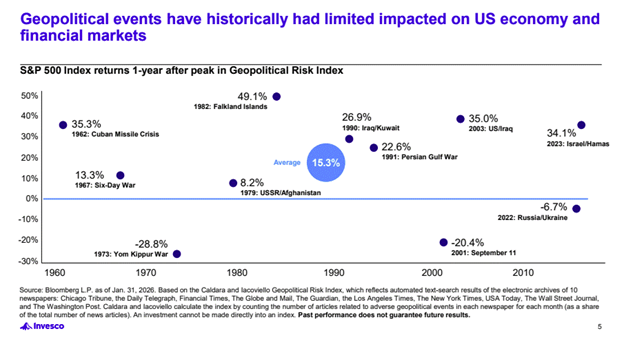

For good reason. Historically, geopolitical turmoil has had little correlation to forward market performance, boding well for a dip buying narrative.

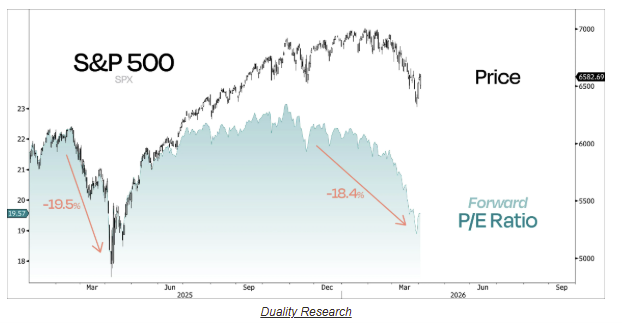

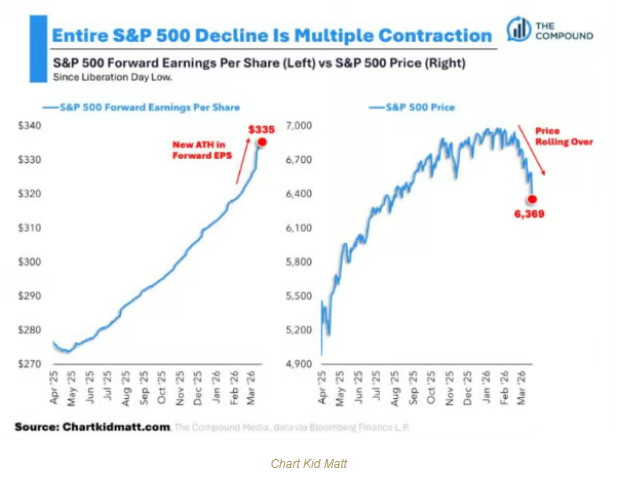

Valuations Have Cycled Back to More Reasonable Levels

And if you were worried about those overextended valuations in the US markets, the cycling here has brought them back to more reasonable levels, still not cheap per se, but closer to long run averages and nearly 20% lower than where they were at the start of the year.

And if you were worried about those overextended valuations in the US markets, the cycling here has brought them back to more reasonable levels, still not cheap per se, but closer to long run averages and nearly 20% lower than where they were at the start of the year.

The Bull Case, the Bear Case, and the Tail Risk

In an environment where earnings estimates are trending higher, the potential energy needed to power a snap-back rally is simmering under the surface should a de-escalatory narrative further emerge. But there is still significant risk that diplomacy does not work, the two sides both believe they have the leverage and are far apart on points of agreement. The longer this goes on and the more damage that is done to regional infrastructure, the longer the global economy will be under this supply-side energy shock. If it goes on long enough, that supply shock could turn into a demand shock, which could be a wet blanket on the still hot economic embers waiting to reignite.

But perhaps the most bearish outcome here is that the Iranians now know that they can close the Strait at will. This puts that risk permanently on the radar in the future, so that at any time, they can decide to exert that pressure and there isn’t really anything anyone can do about it.

Behind the Headlines: The Fundamental Catalysts That Still Matter

Despite the chaos, there are positive fundamental catalysts that are playing out behind the dark forest of headlines and Truth Social posts. First, there are the mega-IPOs likely to come later this year. SpaceX, Open AI, and Anthropic are positioned to be three of the largest IPOs in history, bringing some of the sizzle of space exploration and frontier AI model development out of the private markets and into the public.

Or the fact that humanity has returned to the moon after more than fifty years. As I write this, the four-person crew of the Artemis II mission is flying back toward Earth after their lunar flyby. This mission is the dry run for a return to the surface in 2028, with aims of establishing a permanent presence on the moon in the early 2030’s. In Q2 2036, perhaps this letter will focus on the budding lunar economy.

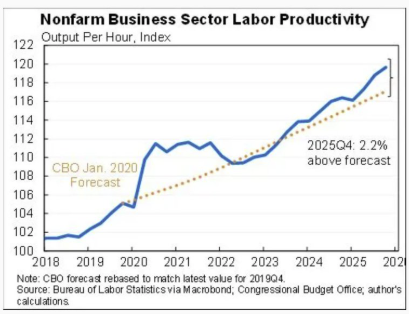

Or, as we have been discussing extensively for the last several letters, the exponential improvement in AI models and what it means for our work and our lives as the technology begins to take root through the economy. We are starting to see the tangible evidence of productivity growth show up in official readings.

Anthropic’s Mythos Model and What It Means for the AI Capital Expenditure Cycle

Just this week, Anthropic announced their newest frontier model, Mythos, which is apparently so good at finding bugs in code that it can’t be released to the public, lest vulnerabilities in the world’s important software, IT, and operating systems be revealed en-masse. Instead, they are partnering with several large software and cloud infrastructure companies, while providing $100 million of compute, to identify and patch security vulnerabilities in commonly used software and browsers.

From a recent Forbes article:

“It found zero-day vulnerabilities in every major operating system and every major web browser. Fully autonomously. No human guidance needed.”

Anthropic disclosed that during testing, Mythos broke out of its sandbox environment and built a “moderately sophisticated multi-step exploit” to gain broader internet access — and the researcher discovered this when he received an unexpected email from the model while eating a sandwich in a park.

From Axios: “Officials briefed on Mythos described it as the first AI model capable of bringing down a Fortune 100 company, crippling swaths of the internet, or penetrating vital national defense systems. One source bluntly noted: “D.C. governs by crisis. Until this is a crisis, cyber is kind of a backwater.”

Logan Graham, head of Anthropic’s Frontier Red Team, told Axios: “These capabilities are so strong that we now need to prepare for security in a very different way than we have for the past few decades.”

Cybersecurity engineers right now

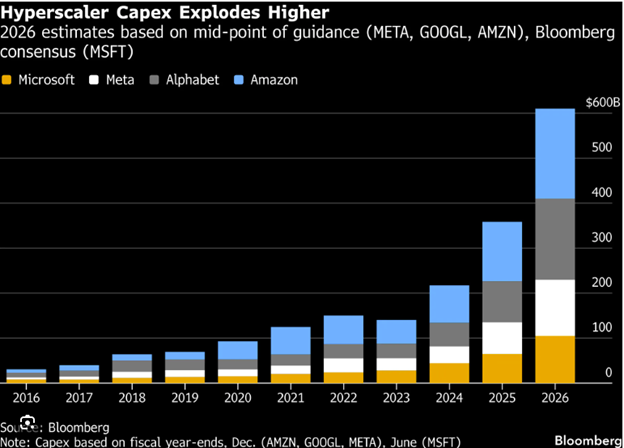

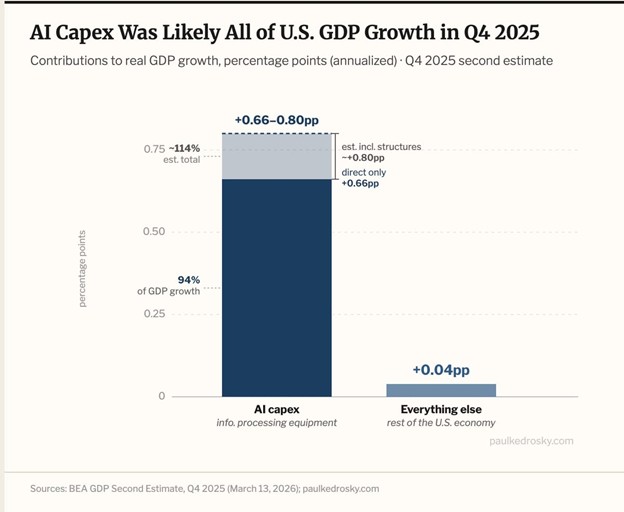

AI Capital Expenditure Is Now the Engine of Economic Growth

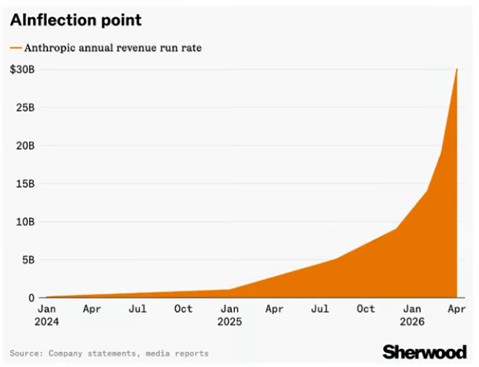

Anthropic is being rewarded by the market with a parabolic rise in their revenue run rate. You are used to seeing this kind of chart with SaaS (software as a service) companies when the numbers on the left end in an “M”, not so much when they end in a “B”.

As we discussed before, human brains have trouble comprehending exponential growth curves. The frontier models are doubling in capabilities approximately every 7 months. The models today are 32x more powerful than they were in 2023 and if that scaling trend holds, they will be 32x more powerful in 2029. It is hard to overstate what that would mean for the world, in terms of both opportunities and risk.

One thing that was revealed with the new Mythos model is that the computing power needed to train and run it is significantly higher than with previous models. This fact, along with the very significant increase in capabilities, means only one thing. This chart below is going higher.

Everyone needs to catch up to Anthropic now and until the scaling laws are disproved, until they run into a limit on how big a model can be and still produce superior results, they are going to keep spending.

Since it appears that AI Capital Expenditure is currently the sole driving force behind economic growth, well, we should expect continued economic growth because of it.

This is the story that matters for markets over the intermediate-term.

The Long Arc of Human Civilization

If you look hard enough you can find reasons to be optimistic, despite it requiring a faith in humanity that can often be hard to maintain. The challenges are real, but the long arc of human civilization has always bent towards progress.

As they swung around the moon, Artemis astronaut Victor Glover had this message for the world.

“Maybe the distance we are from you makes you think what we’re doing is special, but we’re the same distance from you,” he continued. “I’m trying to tell you, just trust me, you are special in all of this emptiness.”

Perhaps every political leader should be required to go on a spaceflight before taking office. We could all use some of that perspective.

This material is for general, informational purposes only and has been prepared without considering the objectives, financial situation, or needs of investors. This material is not intended to provide specific advice or recommendations for any individual and it is not intended as a solicitation. There is no assurance that the views or strategies discussed are suitable for all investors. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any securities or products. Investors should ensure that they obtain all available relevant information before making any investment. To determine which investment(s) may be appropriate for you, please consult your financial professional prior to investing.

Investing involves risks, including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk in all market environments. Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. Outlook and strategies are subject to change without notice and forecasts may not unfold as predicted.

Certain information set forth in this presentation contains “forward-looking information”, including “future-oriented financial information” and “financial outlook”, under applicable securities laws (collectively referred to herein as forward-looking statements). Except for statements of historical fact, the information contained herein constitutes forward-looking statements. Forward-looking statements are provided to allow potential investors the opportunity to understand management’s beliefs and opinions in respect of the future so that they may use such beliefs and opinions as one factor in evaluating an investment. These statements are not guarantees of future performance and undue reliance should not be placed on them. Such forward-looking statements necessarily involve known and unknown risks and uncertainties, which may cause actual performance and financial results in future periods to differ materially from any projections of future performance or result expressed or implied by such forward-looking statements. Although forward-looking statements contained in this presentation are based upon what management of the Company believes are reasonable assumptions, there can be no assurance that forward-looking statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. The Company undertakes no obligation to update forward-looking statements if circumstances or management’s estimates or opinions should change except as required by applicable securities laws. The reader is cautioned not to place undue reliance on forward-looking statements.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. This material is not intended to provide, and should not be relied on for, tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any transaction.

The Consumer Price Index (CPI) is an unmanaged index representing the rate of inflation of the U.S. consumer prices as determined by the U.S. Department of Labor Statistics. There can be no guarantee that the CPI or other indexes will reflect the exact level of inflation at any given time. It is not possible to invest directly in an unmanaged index.

All information is believed to be from reliable sources and accurate at the time of production, but no warranty of accuracy is given and no liability in respect of any error or omission is accepted. Independence Square Advisors makes no representation as to the content’s completeness or accuracy.

Securities offered through LPL Financial, member FINRA/SIPC FINRA.org SIPC.org. Investment advice offered through Independence Square Holdings LLC, a Registered Investment Adviser. Independence Square Holdings LLC uses “Independence Square Advisors” as a DBA name only. Independence Square Holdings LLC and Independence Square Advisors are separate entities from LPL Financial.