As investors, the events of 2020 have forced us to learn an entirely new vocabulary, taking many economists and portfolio managers out of their comfort zone. R-naught values, case fatality rates, incubation periods, and asymptomatic transmission numbers have become more important than future earnings values, unemployment rates, and GDP numbers. Our modern, globally integrated economy has never been so dependent on something health related before and weaving these two worlds together has left markets and their participants in a confused and volatile state. As unprecedented as these events may be, the policy response has been equally so.

This is what happens when an unstoppable force meets an immovable object. We have the worst global pandemic since 1918, the worst economic numbers in terms of employment and GDP since the Great Depression of the 1930’s, and the worst civil unrest since the 1960’s. A seemingly unstoppable force destined to drive asset values down.

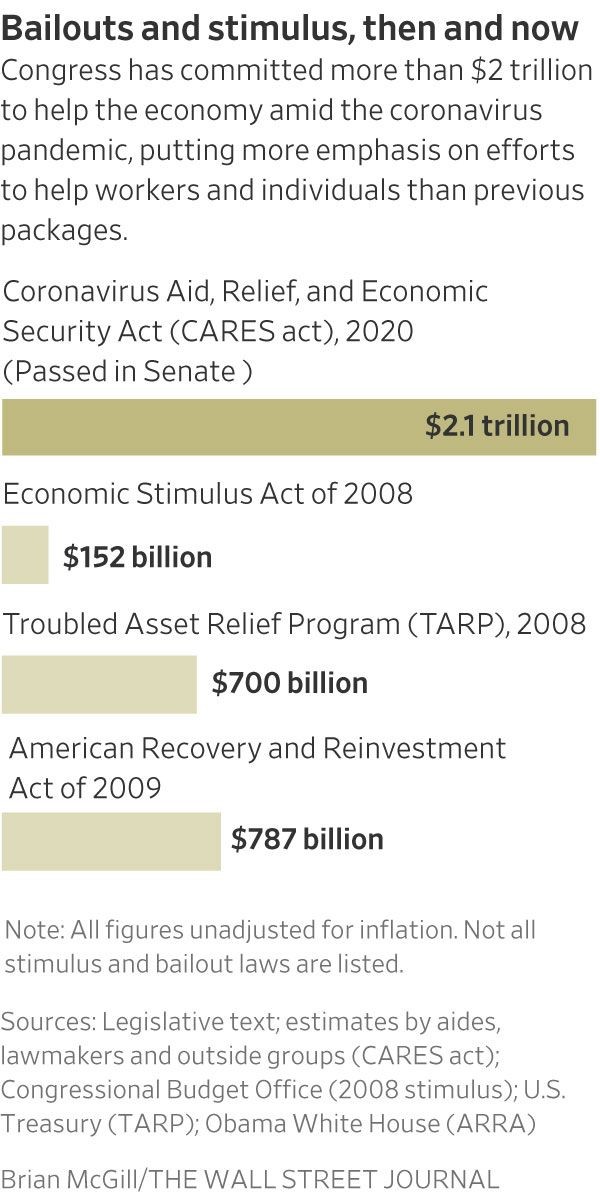

But on the other side, an immovable object. The Federal Reserve, Congress, and massive fiscal and monetary stimulus. The amount of money we have thrown at this crisis significantly surpasses what was employed during the Great Financial Crisis of 2008 and the policy mechanisms being discussed and employed would have been unthinkable in years past. Direct cash payments to citizens, the purchase of ETF’s by the Federal Reserve, and virtually unlimited liquidity are damming the flow of a turbulent economic river. The ‘moral hazard’ has been thrown out the window by the Jay Powell Fed.

The stimulus of the $2.1 trillion CARES Act was triple the size of the TARP legislation in 2008 and was rolled out on an insane one-month timeline. The total $1.5 trillion stimulus response to the Great Financial Crisis took over a year to be passed and implemented.

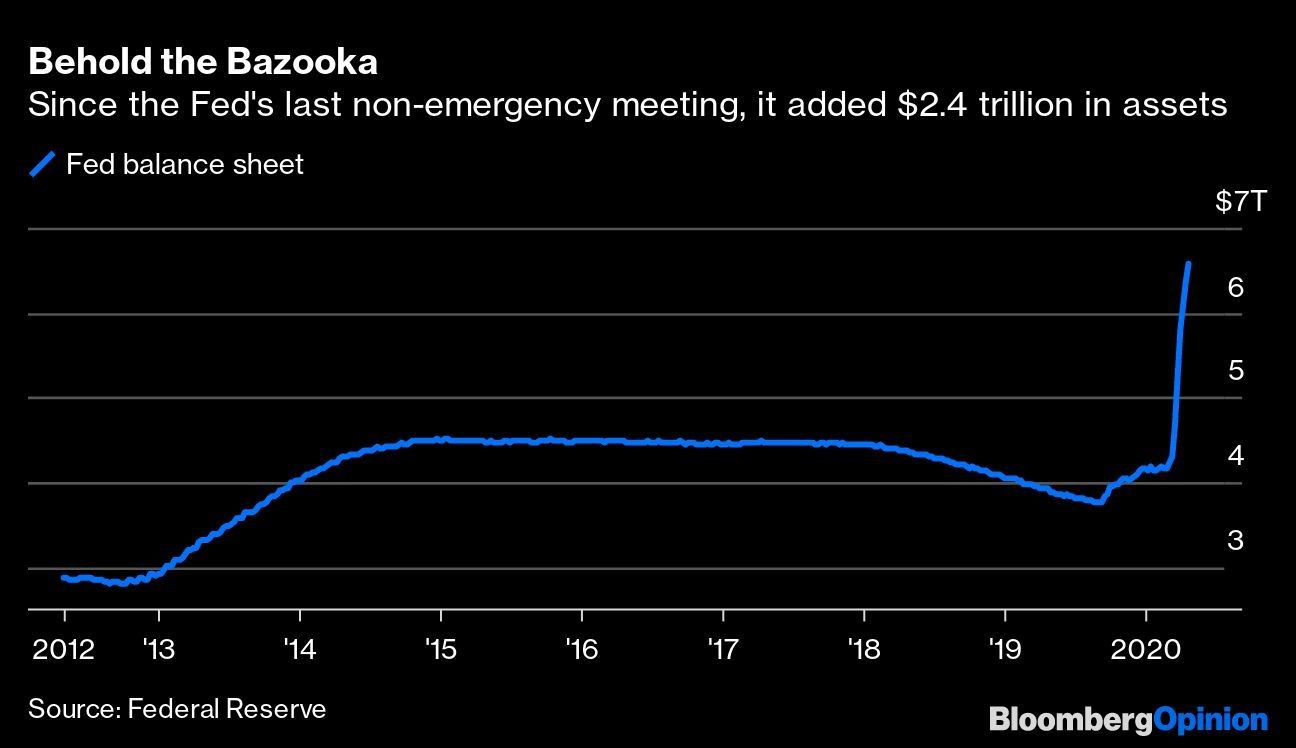

The experiment of reducing the balance sheet holdings at the Federal Reserve has been put on an indefinite hold. It will be years (never?) until it dips back below $5 trillion.

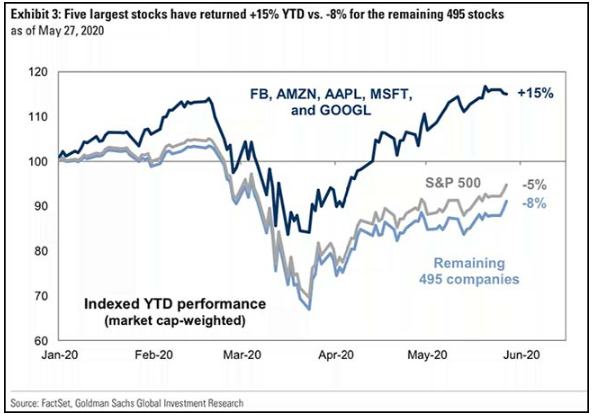

But for everyone who is looking at the S&P 500 each day and wondering how it can continue to rise amid the backdrop of all the negative headlines, the picture is not quite as rosy as it would seem. Yes, with the S&P 500 down less than -5% YTD, it may appear that the market is disconnected from the economic reality, and that may still be true. But when Facebook, Apple, Microsoft, Amazon, and Google have returned +15% YTD through May 27th, while the other 495 stocks have returned -8%, the change in index value may not adequately represent the state of the underlying stocks. If you look at the equal weighted index, the S&P 500 EW has returned -12%. A market down -12% feels much more appropriate to what has been going on versus the modest -5% that the headline may suggest.

The S&P 500 might as well be called the S&P 5 at this point. The index is driven almost entirely by the largest stocks.

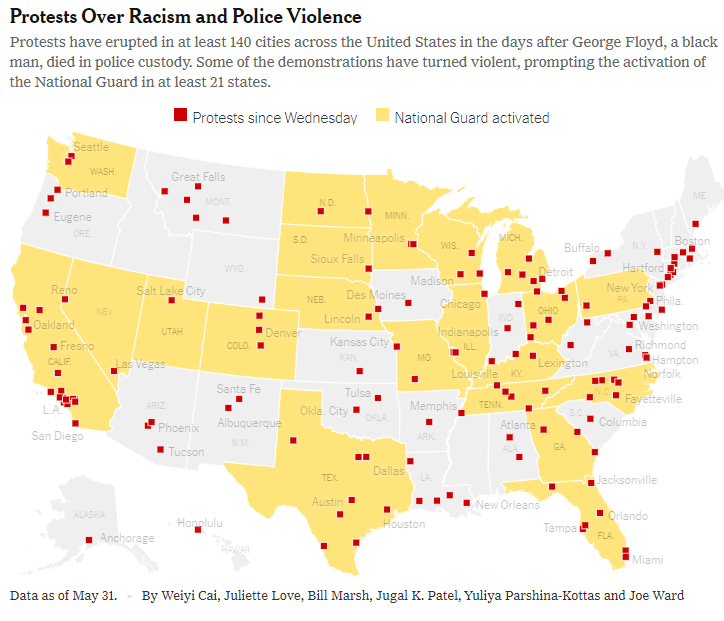

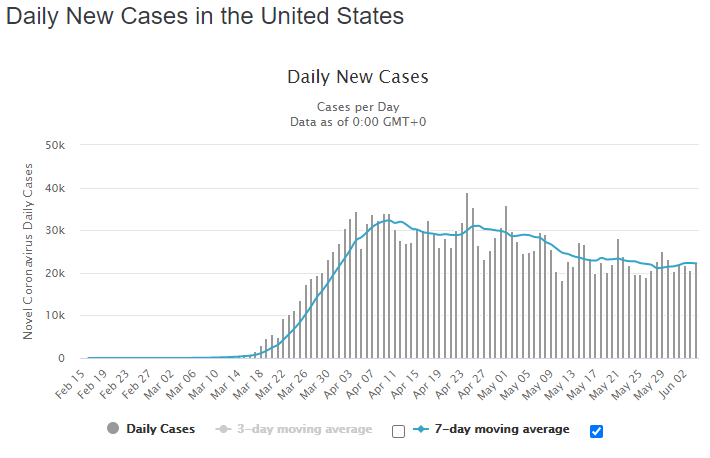

These growing national and now international protests have thrown another curve ball into the equation and gives us a counter-intuitive, perhaps even perverse economic opportunity. Just a week ago, no one in the country could credibly suggest that we would have another mass gathering of hundreds or thousands of people for at least the rest of 2020. We were still limiting gatherings in almost every state to 10 people here, 25 people there. Well, now we have had daily gatherings of thousands of people in almost every city in the country for the last week. In a few weeks’ time, we are going to get a definitive answer on the continued prevalence and danger of Covid-19. If we do not see a massive spike in cases, we can reasonably assume that it will be safe to open the economy, possibly faster than even the best-case scenarios had indicated before these protest movements kicked off. In fact, one of the more restrictive states in Michigan has already rescinded the stay at home order, far faster than anyone would have predicted.

It certainly doesn’t feel like what is happening in the country right now should be supportive to markets, but if it leads to business getting back to business in shorter time frames than would have been otherwise possible, it does make some warped sense. Couple that with trillions of dollars in stimulus, indefinitely low interest rates, and a consumer that has been trapped inside for three months and you can see the bull side of the equation, if (and it is a big if) there is no significant second wave of Covid-19.

We have seen gatherings of thousands of people in at least 140 cities. We are going to get our answer on Coronavirus in the next few weeks by looking at case counts and hospitalizations in these metropolitan areas.

As we have started to open back up the economy, daily new cases have leveled off. If these numbers start to spike again, our governor’s will be forced in to a difficult position of deciding whether or not to re-lock down the economy. These protests have accelerated the timeline on which we will get an answer to that question.