First, the good news. Multiple SARS-CoV2 vaccine trials are showing positive results. The two most notable are from Oxford University and Moderna Therapeutics. Moderna’s phase 1 clinical trial generated a robust immune response in 45 healthy participants and has been deemed safe to move on a larger phase 2 trial of 300 people, with half placed in the placebo group. Given the urgent need, the FDA has already approved a phase 3 trial for this vaccine, which will involve 30,000 people. Oxford had similar success in their phase 1 trial as well, and will also be moving to a parallel phase 2 & 3 trial set.

From a July 14 Time article on the Moderna trial, “All of the participants produced antibodies to SARS-CoV-2, the virus that causes COVID-19. And when researchers tested these antibodies against a lab version of SARS-CoV-2, they found these antibodies neutralized the virus as effectively as antibodies taken from people who were naturally infected with SARS-CoV-2 and recovered.”

These trials are moving very fast, and the federal government is pouring money into the infrastructure behind the scenes that would be necessary to scale up production of a successful candidate. If this Moderna vaccine makes it through phase 3 with similar results as phase 1, we could have hundreds of millions of doses available by the end of the year. That is very good news, but it should still be tempered with a dose of reality.

These were only phase 1 trials, undertaken with a small group of healthy adults between the ages of 18-55. Also, while the vaccine did generate an immune response, we do not yet know how long those antibodies last. Will one need yearly vaccinations or multiple boosters? Will it work on people that are older, immune compromised, or unhealthy? And perhaps the most troubling unanswered question: will the virus mutate and render a vaccine significantly less effective?

Just a few months ago, the most optimistic timelines indicated that it would be 12 to 18 months on the development of a viable vaccine and longer still to get the hundreds of millions of doses produced that we would need to achieve the level of herd immunity necessary to return to normal economic activity. Accounting for these latest developments, we are potentially cutting that timeline down by more than half. An optimistic picture, but not unrealistic. This is what the market has been focusing on. But there is quite a bit that, at least thus far, the market has not been focusing on.

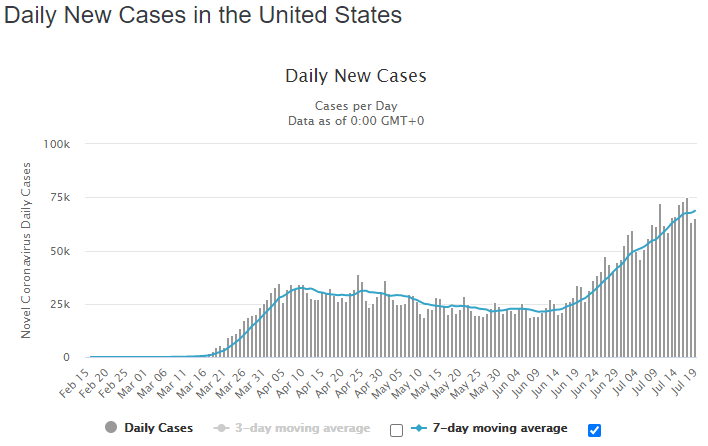

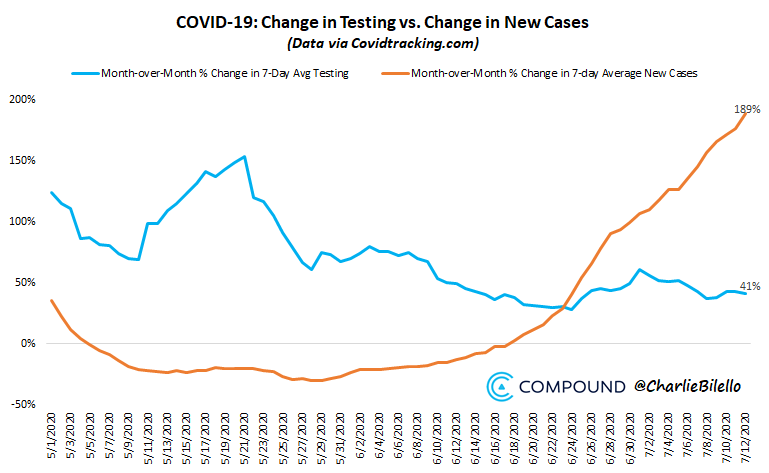

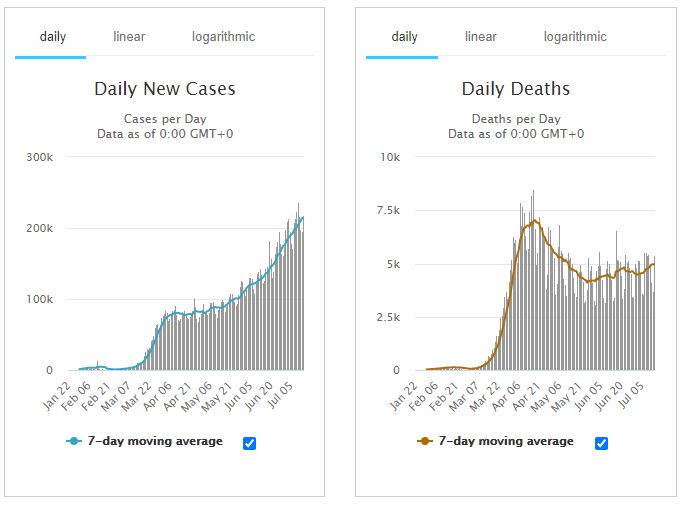

To begin, the confirmed case counts of SARS-CoV-2 have significantly increased in the United States, and it is not just due to an increase in testing as some politicians and pundits have suggested. While the volume of testing has increased by 41% from 5/1 to 7/12, the positivity rate over that time period has increased by 189%, indicating that in fact the community spread of the virus is accelerating in many states.

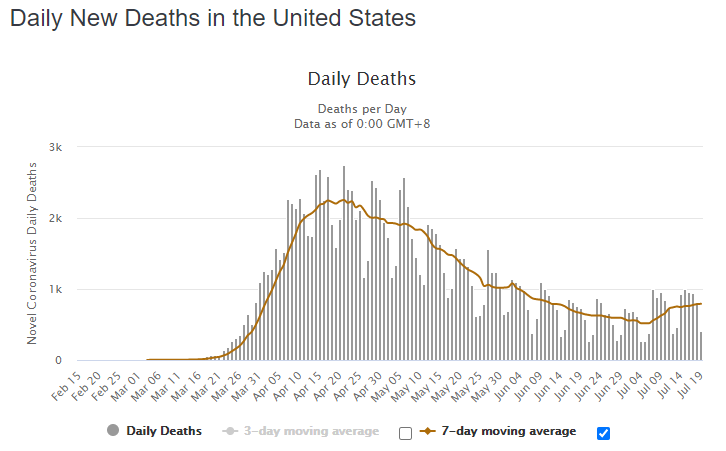

Deaths have also begun to tick up again, but not nearly at the same rate as cases. This is due to several factors, including a lower median age of those recently infected as well as significant improvements in the ability of our healthcare professionals to treat the disease.

These trends are not confined to the US, and the global picture remains grim with over 13 million total confirmed cases and over 600,000 deaths, both exhibiting an increasing trend. We will save the discussion of the ultimate accuracy of these numbers for another time but suffice to say that hundreds of thousands of people have indeed lost their lives directly because of the SARS-CoV2 virus.

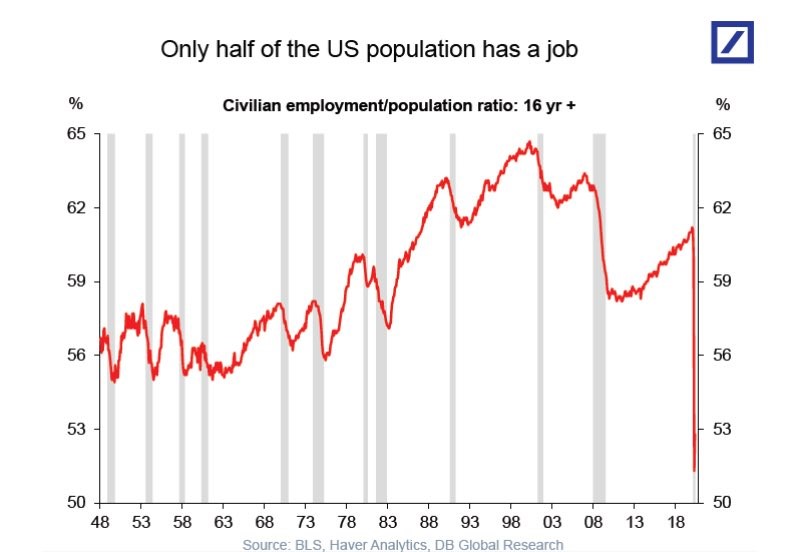

As a result of the health crisis, the economic damage continues to add up. Last week, another 1.3 million people filed for initial unemployment claims, bringing the total since the week of 3/20 to a staggering 51.3 million Americans having filed for unemployment. While the trend does continue pointing down, we are still printing astronomical numbers every single week in comparison to pre-crisis levels. Each weeks unemployment print since March 20th would have been an all-time record by more than double compared to pre-crisis. The breadth of these numbers are hard to comprehend.

Source: 361 Capital Weekly Briefing

This puts us in a position where just over half the US population has a job. The trough dwarfs that of the financial crisis of 2008 and every other recession of the last 70 years. The big difference is that many of these claims are assumed to be temporary in nature, and if we could only return to normal activity, many of these people would be expediently rehired. But until that actually happens, we have to consider them all as potentially “permanent”. It is impossible to say how many ultimately will be and how long it will take after the health crisis recedes to get there.

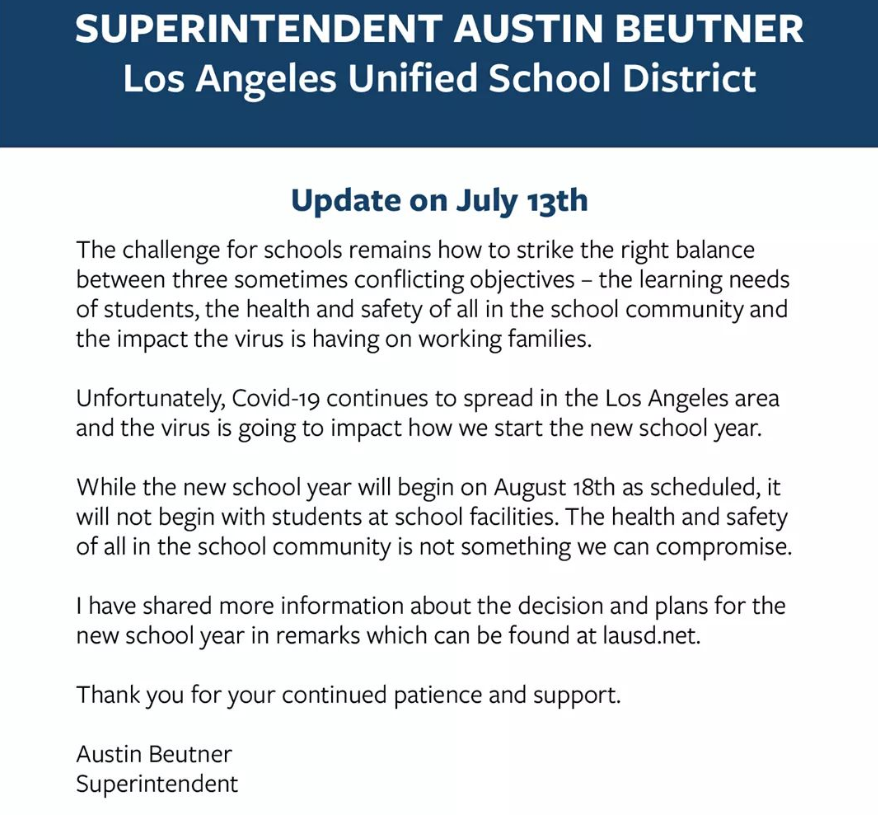

Meanwhile, several states are walking back their reopening plans, sports leagues are going to attempt to salvage their seasons and schools grapple with whether to open in the fall. The largest school district in the country, Los Angeles Unified, has already decided that they will not be physically going back to school as scheduled. This has a huge impact on families and businesses in the area.

Finally, we are up against a deadline at the end of the month of expanded unemployment benefits running out and PPP loan money running dry in small business bank accounts. Congress may (must) act to pass additional stimulus before the summer recess, but it may not be as easy and bipartisan as it was back in April when the market was in freefall, the election more than six months out, and the health picture far more bleak.

Investors are clearly focusing on the first part of this article and the prospects for a speedy vaccine development timeline. Perhaps that will come to fruition and we can look back on these times by the Christmas shopping season as a crazy few quarters where the world was turned upside down. But perhaps there is still a reckoning to come with the economic reality and our optimism will be proven misplaced.

Securities offered through LPL Financial, member FINRA/SIPC. Investment advice offered through Independence Square Advisors, a registered investment advisor. Independence Square Advisors is a separate entity from LPL Financial.

Forecasts may not unfold as predicted. The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.