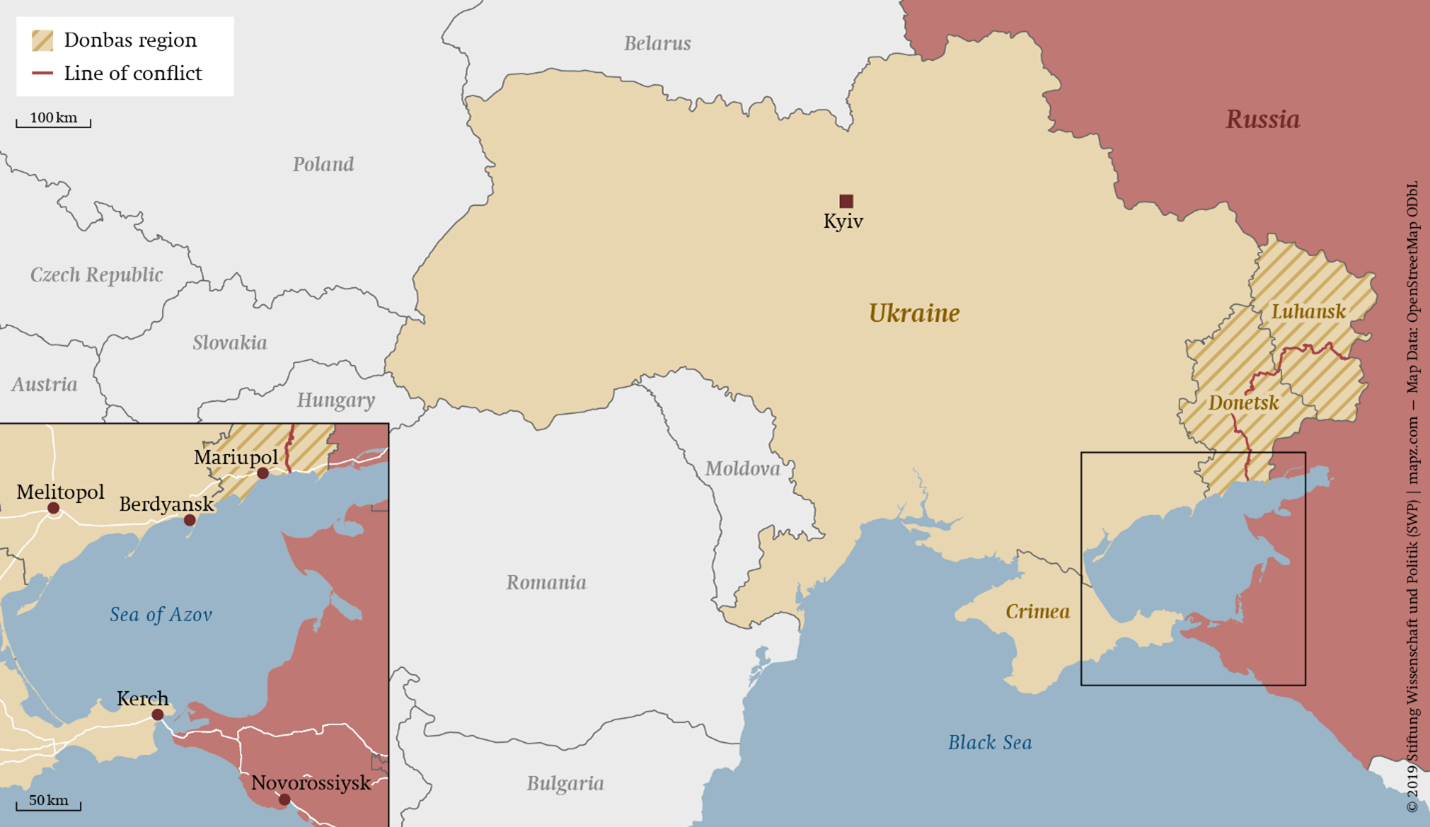

As was largely expected, Russia engaged in offensive military action against Ukraine today. It is unclear at this time what the extent of the incursion will be and what the goal of the Kremlin is. For a context of where this is happening, we can turn to the map below. Since 2014, there has been fighting in the Luhansk and Donetsk regions of eastern Ukraine between Russian backed separatists and Ukrainian forces. Russia also annexed Crimea in Southern Ukraine in 2014. A majority of people in the Donetsk and Luhansk regions are ethnically Russian and Russian speaking. Many analysts expect a Russian annexation of these regions after the Kremlin declared them “independent states”, but that a long-term occupation of the entirety of Ukraine would be much more difficult and unlikely operation.

Before discussing the market impacts of these events, let’s examine a piece of broader market context. Prior to this correction, there hadn’t been a single 5% pull back since September of 2020. Typically, you can expect 3 of them a year. Prior to 2021 and 2017, the last year without a single 5% pull back was 1995. 2021 was an abnormally low volatility year with a significantly above average return. We were well overdue for some of that to be given back.

While we are discussing economics and markets here, we do want to recognize the real human suffering of the people in the path of this conflict and the lives that are lost and overturned. For any of you reading that have family and friends in harm’s way, our thoughts are with them.

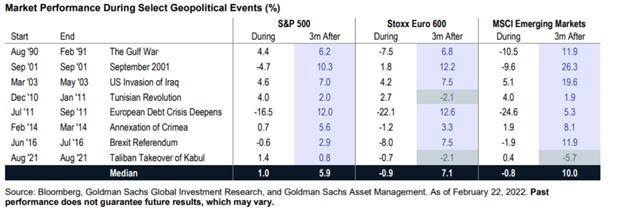

When it comes to the impact of today’s events on our investments and global economy it is important to separate out the market impact and the economic impact. As we are seeing, any geopolitical event on this scale will produce a volatile market reaction and as long as the uncertainty around the eventual outcome remains, we can expect heightened volatility in global markets. However, absent a larger war with other European countries or NATO, we expect any longer term or substantial impact to markets and the global economy to be small. Below we can see the table of other geopolitical events of the last 30 years and the impact on the markets. In none of them was the S&P 500 negative three months after the conclusion of the events.

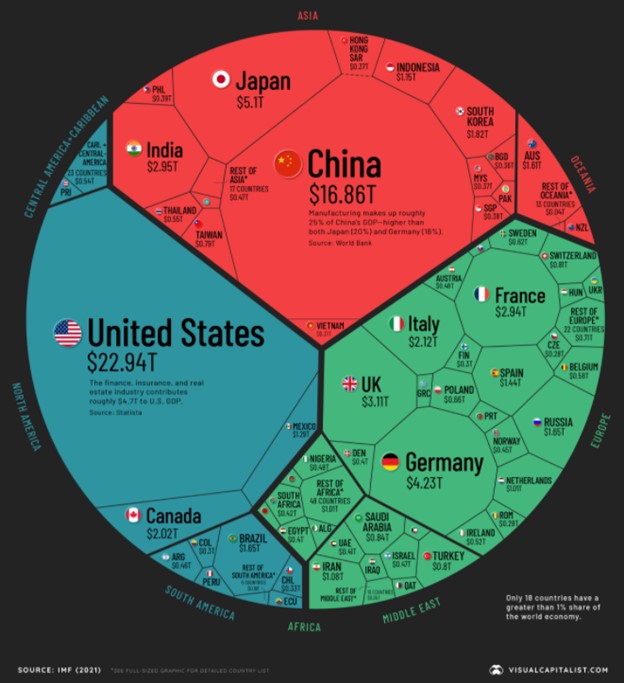

Russia accounts for around 3% of global GDP, while Ukraine accounts for 0.4%. Neither country is a particularly large trading partner of Europe or the United States and during the last episode in 2014, the impact on financial conditions in Europe was limited. The chart below offers an easily digestible visual representation of the size of the world’s economies.

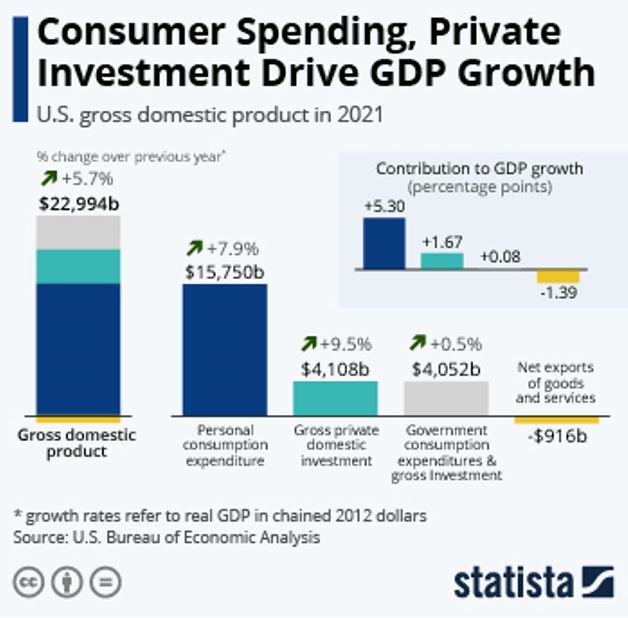

We do not expect any significant impact of this conflict on the fundamentals of the global economy and especially not the domestic economy. Almost 70% of our US GDP is driven by domestic personal consumption. This is assuming that there is no direct conflict between NATO and Russian troops. That would be a paradigm shifting event and remains a very unlikely possibility in our opinion.

We do expect more significant impact in the energy markets, especially European gas markets, as Europe does receive around 40% of its gas from Russia. This could have knock on effects across the global energy complex as supply is constrained, potentially further fueling already high inflation.

The biggest unknown is how the Federal Reserve will react to potentially higher inflationary pressures at their next meeting in March. Whether they stay on their current path or change course remains to be seen. We still believe that a policy misstep by the Fed remains the biggest risk to our domestic economy.

Securities offered through LPL Financial, member FINRA/SIPC. Investment advice offered through Independence Square Holdings, LLC, a registered investment advisor. Independence Square Holdings, LLC and Independence Square Advisors are separate entities from LPL Financial.

All indices are unmanaged and may not be invested in directly. Economic forecasts may not unfold as predicted. The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results.